14: My Thoughts on Roper, How MS Flight Simulator Built the World, and Oracle + TikTok?!

"If Oracle won, I think it would very much be the proverbial dog that caught the car."

A good teacher will arm you with the tools to dispute their conclusions. —The Stoic Emperor

It’s been almost a months since I launched this thing. I think I’ve learned a few things going up the learning curve, but I’m sure there’s yet much further to go.

If you have feedback on both things you like and dislike, don’t hesitate to reply to this email and drop me a line, or DM me on Twitter.

Investing & Business

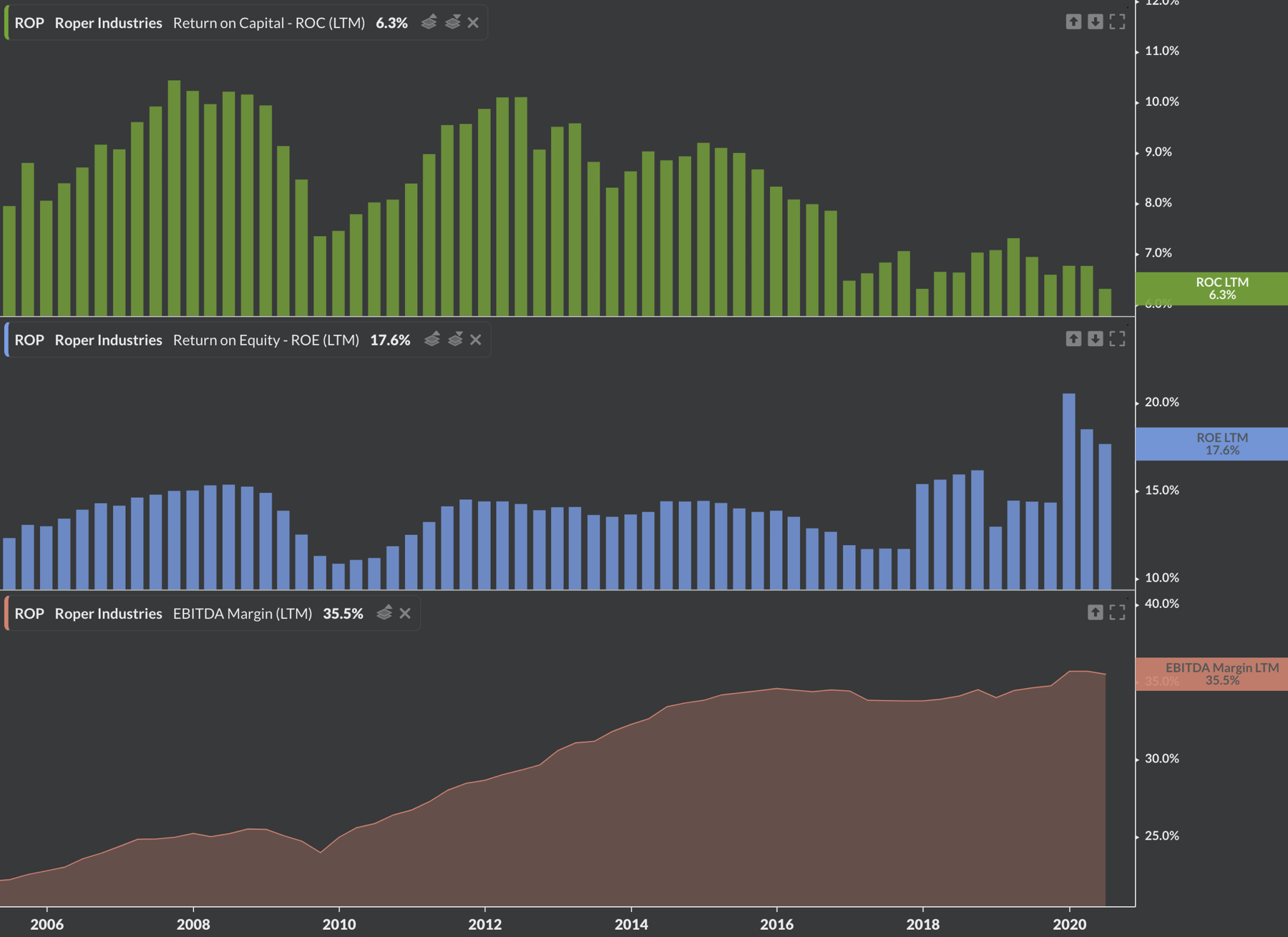

Some Thoughts on Roper

Randomly got into a conversation about Roper ROP 0.00%↑ on Twitter, and it made me think about the company’s model (again). I’d like to share some of these thoughts here.

So an observer may look at the financials and see that ROIC has been going down over time. For an acquisitive company like Roper, this look like a bad sign. They’ve done well in the past, but what if lately they’ve been paying more for acquisitions and the future returns are much lower because of that? Have they just lost their touch, or have others caught up to their model and crowded out the market?

My first thought: if Roper was a stable business, doing the same thing over and over again (buying the same kind of companies, like rolling up an industry), or if they were not acquisitive, it would be alarming to see ROIC go down over time.

But ever since Brian Jellison (RIP) joined about 20 years ago, the company has been transforming itself. It went from an industrial conglomerate making pumps and various oil & gas equipments to a collection of much better businesses (where quality is defined by things like predictability/recurring revenues, high margins, low competition in a defensible niche, higher terminal value, very low need for capital & assets to grow, low or even negative net working capital, differentiated/custom products and services, etc).

So if your gross/EBITDA/FCF margins are going up year after years, and your capex as a percentage of revenue is going down, and your ratio of recurring revenues is going up, etc, it’s only normal for the market to give you a higher valuation. Which is exactly what has happened.

But it’s also normal for the assets that you’re buying to have higher multiples too. For a company that deploys pretty much all its free cash flow into M&A (levered conservatively to 2-3x turns of EBITDA), it’ll make it look like your ROIC is going down over time.

That’s because you used to pay less for worse businesses, and now you pay more, but for better businesses. That makes the ROC look like it's going down, but the value created may not be be going down, or at least, not at the same rate as the ROIC (because size does eventually make it harder to deploy capital — ask Buffett). That’s where you need to analyze things and make judgement calls.

Is that easy to keep track of and model in a spreadsheet? No. But who said it had to be? Where is it written that all the important insights about a company need to fit in a model… It’s the whole “I’d rather be approximatively right than precisely wrong” cliché.

Because Roper runs levered, looking at the ROE may be more indicative of how the collection of assets is performing (and it’s currently doing well), while looking at ROIC ex-intangibles may give you a better indication of how the quality of the assets is evolving (though not of the returns that you’ll get, since you haven’t gotten them at that price, but it’s a proxy for how defensible these assets are, since if they weren’t, someone with very little capital could set up shop and compete away the margins and returns).

In the end, I think looking at FCF/share while monitoring the quality of the underlying businesses, the culture, and M&A discipline is a better indicator of progress than ROIC for the entity as whole.

Of course, I may be wrong about all this, but this is kind of how I’ve been thinking about it.

Would it be better if they were able to buy assets at 25-30% unlevered ROIC like Constellation Software? Sure. But these assets don’t exist with the type of strategy Roper is running. They don’t have expertise doing hundreds of tiny deals and they don’t do turnarounds. Everyone has to know what they’re good at and not try to do everything, and select the risks that they’re best able to handicap and deal with while focusing on what they’re good at.

Roper is trading-off a higher hurdle on individual acquisitions for much more capital deployed into attractive, predictable businesses that they lever up conservatively to get decent returns.

Over its whole run, Constellation hasn’t deployed as much capital as Roper has deployed over the past year (from memory). Life is about trade-offs.

Heico Acquires Niche Embedded Computing Company

Heico’s Electronic Technologies Group announced a new acquisition this morning:

Electronic Technologies Group acquired 89.99% of Connect Tech Inc. (“CTI”) for cash at closing, plus potential additional cash consideration to be paid if certain post-closing earnings levels are attained. Further financial details were not disclosed. [...]

Connect Tech designs and manufactures rugged, small-form-factor embedded computing solutions and offers both standard commercial off-the-shelf products, as well as custom design services. CTI is well-regarded for its computer-on-module carrier boards and GPU solutions. CTI is NVIDIA’s largest global embedded hardware partner, for which it is an NVIDIA® Jetson Elite Partner. CTI’s components are designed for the harshest environments and are primarily used in rugged commercial and industrial, aerospace and defense, transportation, and smart energy applications. (Source)

The business is based in Guelph, Ontario, Canada. Founded in 1985. HEI 0.00%↑

‘Plumbing the World’s Markets: The Story of ICE’

I enjoyed this piece by Marc Rubinstein on Intercontinental Exchange Inc ($ICE), which provides nice context on their recent acquisition of Ellie Mae from Thoma Bravo:

Intercontinental Exchange Inc. (ICE) and its founder and CEO, Jeff Sprecher, has made a career out of analog-to-digital conversion. He’s done it in energy trading, he’s overseen it in equity trading, he’s doing it in fixed income trading and now wants to give it a go in mortgage. [...] Having installed the plumbing for some of the world’s biggest markets, will Jeff Sprecher be able to do the same for mortgages?

Many entrepreneurs become wildly successful on a single, valuable insight. Others have several. Jeff Sprecher is one of those that has had several. I count three:

The first is the analog-to-digital shift. [...]

The second insight is to see regulation as an opportunity. [...]

The final insight is the value of data. [...]

The Ellie Mae acquisition raised questions about valuation. The company had traded less than 18 months earlier at a third of the price ICE is now offering to pay. Partly that’s because the business has performed better than expected. At the time of the first deal, management anticipated US$620 million of revenue in 2020 and US$201 million of EBITDA. The company now anticipates US$900 million of revenue in 2020 and US$470 million of EBITDA. Partly it’s because risk has been reduced, with Ellie Mae having successfully migrated to the cloud.

You can read the whole thing here. ICE 0.00%↑

Cablecos to Bid on Spectrum Just to Mess with Telecos?

Good thoughts on cable companies and their rivalry with wireless companies by Andrew Walker. This passage stood out:

The CBRS auction is going on as we speak. Most people think Verizon is going to take the lion's share of that spectrum, and maybe they will. But if you're cable, I think you look at that spectrum and think "hey, that would work really well on our network if we started installing a lot of small cells. Why let Verizon have it? Let's bid aggressively on it; if we win it, great! If not, let's make Verizon pay a price that precludes them from thinking about building Fiber to the Home because they've spent way more than they wanted to on spectrum and now they're prioritizing debt paydown."

It’s win-win, except both possibilities of winning are on the cable side, and the telcos lose either way (either they pay more than they would’ve, or they lose spectrum that they need and get more wireless competition from well-funded rivals). VZ 0.00%↑ CHTR 0.00%↑ CMCSA 0.00%↑ T 0.00%↑

Oracle Trying to Buy TikTok?!

2020 is weird. Now it’s Oracle that is apparently trying to buy the U.S. operations of Tiktok:

The tech company co-founded by Larry Ellison had held preliminary talks with TikTok’s Chinese owner, ByteDance, and was seriously considering purchasing the app’s operations in the US, Canada, Australia and New Zealand, the people said.

ByteDance is opposed to selling any assets beyond those in the US, Canada, Australia and New Zealand, said a person close to the company. (Source)

If Oracle won, I think it would very much be the proverbial dog that caught the car. It wouldn’t know what to do with it. I doubt experience running on-prem databases help run a consumer product targeted at teens, or that high-touch enterprise sales is much help in selling TikTok ads.

This isn’t just about hosting the app and paying for its bandwidth costs. You need ongoing development of the algorithms and user experience (new features, respond to competitive threats) to keep the thing going and growing. And because it is user-generated content and social, you need a bunch of human moderators to deal with issues (in multiple languages, even just within the countries that are reportedly for sale).

Microsoft is already a bit of a stretch because of their enterprise focus, but they have experience with consumer products and services, and they have a lot more machine learning talent (which is the secret sauce for TikTok) and a top 5 tech CEO that has shown the ability of giving autonomy to acquired businesses and not ruin them (Mojang/Minecraft, LinkedIn, Github). I wouldn’t be surprised if Nadella was able to create an environment within Microsoft that allows TikTok to do its own thing well.

Oracle was working with a group of US investors that already own a stake in ByteDance, including General Atlantic and Sequoia Capital, the people added.

This seems like a fairly transparent ploy by Bytedance and its major investors to extract a higher price from Microsoft by having a second serious bidder that has resources (Twitter was just too small and didn’t have the warchest — Oracle has over $40bn in cash on the balance sheet and has huge free cash flows).

Job Losses During Post-War Recessions

Science & Technology

Microsoft Flight Simulator: 1982 -> 2020

From this:

To this:

It’s really interesting how they leveraged other assets at Microsoft and from smaller companies doing AI/ML mapping and past research projects to have basically the whole planet available to fly over, in great detail (including realistic weather):

Around six years ago, he was working on a product called HoloTour for Microsoft's HoloLens augmented reality headset. "And that's basically what inspired Flight Sim because you can't build Machu Picchu, right?" he told Protocol. "You can build all the buildings and roam on a street level, but Machu Picchu is this sprawling mountainside and endless vistas. So I ended up talking to the Bing Maps team and they had the entire planet. [...]

For HoloTour, Neumann was working with Asobo Studio in Bordeaux, France, which had developed a graphics engine specialized for huge virtual environments. Neumann discovered that the Bing team had detailed photogrammetry data down to 5-centimeter resolution for more than 400 cities. Microsoft contracts with various providers around the world, such as Vexcel Imaging, to fly all over the world using technologies including lidar (a laser version of radar), to generate imagery and models of the real world. [...]

Microsoft didn't have detailed photogrammetry for the whole planet, though, so it had to use proprietary satellite imagery in addition to traditional aerial photography. That's where a company called Blackshark.ai in Graz, Austria, came in. It just so happens that Bing's camera technology had been developed at a university there, and the town is home to a community of vision scientists. [...]

Neumann went to Switzerland to meet with some hardcore weather nerds about incorporating their models into the product. "They can tell us stuff like the altitude ice condensates at under various conditions," he said. The team also leveraged technology from Microsoft's discontinued Photosynth project, which generates 3D models from 2D photos.

The algorithms and data — including OpenStreetMap — were then fed into Microsoft's vast Azure computing cloud to generate Flight's 2.5-petabyte model, which includes 2 trillion trees, 1.5 billion buildings (you can probably find your house), 117 million lakes and just about every road, mountain, city and airport on the planet.

It’s just bonkers! You can read the whole thing here. H/T @JerryCap MSFT 0.00%↑

Primer on Asteroid Mining

The Winklesvoss Twins tried to convince Dave Portnoy to buy Bitcoin rather than gold because Elon Musk may decide to mine asteroids and crash the price of gold…

While that’s kind of a *deep bong rip* argument to make, asteroid mining is likely to happen at some point in the future because, well, it actually makes sense once you reach a certain level of technological development.

The talented folks at Kurzgesagt (“In a Nutshell” in German) just released a new short animated video about it. I recommend it:

Stripe Engineers on Building Machine Learning Infrastructure

I enjoyed this episode of Software Engineering Daily. It’s an interview with Kelley Rivoire and Rob Story, two engineers working on machine learning infrastructure at Stripe.

One of the most interesting thing about humans is our tools. And the people who make tools to help others make products and/or tools stand at a high-leverage point in the value chain.

If you can create tools that make almost every other engineer in a R&D-focused organization more productive, or creating training methods and reference documents that make almost every sales person in an organization better at sales, etc… That kind of upstream work should be very interesting to anyone who likes to think about the systems at play in an organization.

After recognizing the difficulties that engineers faced in creating and deploying machine learning models, Stripe engineers built out Railyard, an API for machine learning workloads within the company.

More details on Railyard here.

You can listen to the interview here. I’d rate it at “medium” on the “how technical is it” scale, but even if you don’t understand everything, I’m sure you’ll understand and learn something.

And if you want more, I’ve also found this other interview with Rivoire on the This Week in Machine Learning podcast, but I haven’t heard that one yet.

The Arts

1946 Edition of Gibbon’s Decline and Fall of the Roman Empire

I’ve always liked the design of this edition.

Created by Clarence P. Hornung, the design captures the essence of Gibbon's classic, showing Roman pillars progressively crumbling as your eyes move from Volume 1 to Volume 7. (Source)

May I ask which software you use to produce those really nice looking Roper charts?