619: Constellation Software Q4, Who Would Buy AMD, Anthropic Amicus, Ground Robotic Warfare, Lithium Deficiency and Alzheimer's, GPS Spoofing, and New Rembrandt

"belongs among the moral catastrophes"

It is better to examine one’s own faults than those of others.

—Democritus

🤰🌎💣 I’ve had a draft for a while about the damage done by Paul Ehrlich, his acolytes, and the whole “population bomb” memeplex from the late ‘60s and ‘70s. I was going to write a whole thing, but then I saw the letter above, and thought, well, that says it better than I could.

I think these ideas — which were too often closer to ideology than analysis — did serious damage. Some of it was direct and visible. Many tyrants used them to justify campaigns of forced sterilization, one-child policies, and other coercive demographic engineering. That sounds clinical, but I’m talking about real people and real families. India’s Emergency-era sterilization campaign involved millions of sterilizations, many of them forced. China’s one-child policy was enforced through forced abortions, forced sterilizations, and other severe abuses. It likely prevented an enormous number of births, with estimates typically ranging from 200 million to 400 million. Variants of the same nightmare showed up all over the world. 🚫🤱

But there’s also the less visible damage, which may be just as large: the broad voluntary adoption of these ideas by ordinary people persuaded by arguments that sounded plausible and scientific and turned out to be badly wrong.

When you add it all up, both the visible abuses and the downstream effects, I think this ideology belongs among the moral catastrophes we don’t talk about enough. Not because the harm wasn't real, but because of the difference between sins of omission vs sins of commission.

Killing millions of people makes the history books, with photos of the battlefields and bombed-out cities, and detailed reports of what happened.

Making millions of people never even be born through persuasive but flawed arguments doesn't get coverage. It's almost like that time-surgeon scene in Looper when they start carving up Seth's past body, and you watch his future self disappear, limb by limb, killed from the past (I still get shivers down my spine from that scene 😬).

🔎📫💚 🥃 We’re at the point where too few readers of this newsletter are paid supporters, and it’s threatening the existence of the project.

Don’t take it for granted. If you want it to continue, become a paid supporter 👇

🏦 💰 Business & Investing 💳 💴

✨ Constellation Software ✨ Q4 2025

The first quarterly conference call since *checks notes* February 2018 is worth noting.

Results seemed pretty solid to me, especially if you focus on cash flows and owner economics rather than on messy IFRS numbers. A lot of the accounting noise comes from minority stakes and the IRGA/TSS liability that gets constantly marked-to-market (to understand it better, check out what friend-of-the-show Leandro wrote about it) and large amortization charges from M&A that most shareholders would not treat as reflective of economic reality.

The headline numbers are:

Q4 Revenue: +18%

Q4 Organic: +6% (2% ex-FX)

Q4 Maintenance & recurring organic: +9% (6% ex-FX)

Q4 Cash flows from operations: +16%

Q4 capital deployment: $571 million

Q4: “Other net investments of $321 million were completed, including the Company’s net investment in Asseco Poland S.A.” (Asseco is via Topicus, but they are also investing in Sabre and possibly other public companies that haven’t been disclosed yet)

But that’s not all: “Subsequent to December 31, 2025, the Company completed or has open commitments to acquire a number of businesses for aggregate cash consideration… of $802 million.” 😲

FY25 Revenue: +15%

FY25 Organic: +4% (3% ex-FX)

FY25 Maintenance & recurring organic: +6% (5% ex-FX)

FY25 Cash flows from operations: +24%

FY25 capital deployment: $1.58 billion

FY25: “Other net investments of $530 million were completed, including the Company’s net investments in Asseco Poland S.A.” (so total deployed in 2025 topped $2bn)

I want to share my highlights from the conference call with Mark Miller, who is technically President and COO, not CEO. Constellation never really used the title of CEO, Mark Leonard was always just ‘president.’

First, on their renewed interest in doing public market investing, which they clearly are serious about because they gave it a memorable name and Mark Leonard is involved (I hope he’s doing well):

Mark Miller: We’ve also developed a new approach to deploying larger amounts of capital, what we’re calling a Permanent Engaged Minority Shareholder strategy or PEMS.

Our investment in Sabre is the first meaningful expression of it. And I have to thank Mark Leonard who is helping us with this strategy and helped us explicitly on this particular investment.

But the logic is straightforward. Permanent, meaning we’re long-term holders, not traders. We’ll work to ensure these companies endure as institutions. We’re engaged, which means we care about governance, management incentives and capital allocation, and we’ll actively work to have an influence where we think it creates value. Minority, we’re not acquiring these businesses outright. We want to partner with other shareholders, and we hope many of them become engaged long-term holders alongside us.

I’m sure they’d be flexible on the ‘M’ part of the acronym if the opportunity presented itself to acquire in full one of those investments 🤔

I do like the ‘E’, though, because most software companies are VERY different from Constellation. They have tons of SBC and far less focus on profitability and ROIC. If they can identify assets with potential but bad strategies, and go activist-lite on them and guide them to make better decisions, it could become a kind of self-catalyst for their investments. But it remains to be seen if the targets will want to listen to a minority holder. If they were smart enough to listen, they may not be in the trouble that will make Constellation interested in the first place 🔁

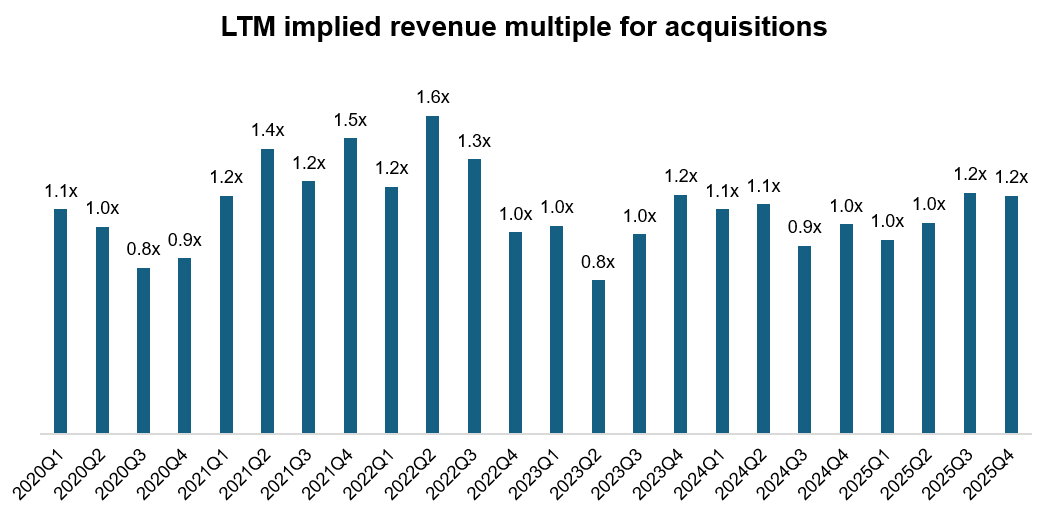

Public market investing is something they used to do in the company’s earlier days, and I don’t think they stopped because they were ever against the idea on principle or anything, it’s just that public VMS valuations kept going up as private acquisitions stayed more reasonable.

In fact, this graph by my friend MBI (🇧🇩🇺🇸) shows the implied revenue multiples paid for acquisitions in the past few years. The 2021 software bubble is barely visible here, unlike if you look at almost any software company’s historical multiple graph:

The advantage of public companies is clearly capital deployment at scale, because it’ll always be hard to beat deploying money around 1x sales and roughly 3-5x post-improvement EBITDA.

They announced an $80 million investment in Redknee, a public VMS, in December 2016. ESW Capital outbid them eleven days later. Constellation declined to match, collected a $3.2M termination fee, and that was that.

Back in 2015, Mark Leonard wrote in his annual letter:

During the period from 1995 to 2011, we made sixteen public company investments in the software sector.

If you viewed our public company investments as a single portfolio, the internal rate of return (”IRR”) for that portfolio far exceeded our hurdle rate. Thirteen of the sixteen investments generated individual IRRs in excess of 10%, and only one small investment had a negative rate of return.

The average hold period was shorter than we would have liked, and most of the investments ended in the companies being acquired by third parties, rather than CSI. Those may prove to be the fundamental limitations for this sort of investment activity. We hope to find some attractive public software company investments in the coming year or two.

At present, the pickings are slim due to generally high valuations.

It’ll be interesting to see if the PEMS strategy becomes a new pillar for a while, or if it’ll also be just a temporary window.

I suspect the opportunity will be around for a while because the AI overhang on software isn’t going away any time soon, and there will be babies thrown out with the bathwater for a while. That may represent an opportunity for a discriminating allocator. The company has added an “explicit AI lens” when assessing acquisitions, and I assume they’re doing the same in the public market.

The next interesting bit is about what they’re seeing so far when it comes to AI disruption:

Mark Miller: So there’s a real noise in the market now about AI disrupting software businesses, and we take that very seriously. But we think we’re well positioned, although we’re staying very disciplined about how we approach it.

We’ve always run a learning culture at Constellation. Best practice sharing across our operating groups is one of our genuine differentiators. And I’ve seen more cross-portfolio collaboration around AI in the past year than on any topic in recent memory. Over the past 12 to 24 months, we’ve directed our culture of best practice sharing to helping our businesses navigate the AI transition thoughtfully.

We spent 2025 upskilling our development teams. Thousands of developers have built skills in AI augmented coding across our operating groups. We’re entering 2026 with AI-enabled coding becoming increasingly commonplace. The productivity returns are real, and they’re still growing as these skills embed more deeply in our business units across the world. [...]

But I want to be direct about something, building products and features faster will not be what differentiates us long term. That capability will become widely available. It’s going to be table stakes. What will matter is what our businesses have spent many years developing, deep vertical knowledge, a genuine understanding of customer workflows and processes, the data inside their solutions and the trusted relationships they’ve built. I believe AI will help us do all of this better.

When I look at where this leads, the opportunity I find most interesting is what I described as knowledge networks, connecting our domain expertise, customer process knowledge and data assets in ways AI now makes possible. That’s a long-term build, and we’re in early days, but the foundation is real.

Our customers rely on us for mission-critical software. We believe that the trusted partner position we’ve earned in our verticals is now extending to guiding them on how to safely and effectively bring AI into their own businesses.

That’s the upside.

What about the downside, Mark?

Mark Miller: Yes, we haven't really seen a lot of new revenues from that, right, so far. And on the converse, we haven't seen loss of revenues from it, at this point.

He was also asked if customers are pushing back on pricing, and he said there’s no change there either.

This doesn’t mean it can’t change in the future, but so far, despite the big moves in stock prices, they’re not seeing much on the ground.

The last thing I’ll mention is their evolving views on buybacks. They’ve gone from a pretty definitive ‘no’ under Mark Leonard to saying that they now have a board sub-committee looking at it and have a ‘number’ at which they would do it.

Considering the kind of hurdle that they have for deploying capital, and how conservative they are in modeling things, I suspect they probably won’t hit that number. They don’t typically give credit for future growth, which is a big difference between Constellation, which has a capital redeployment engine, and the VMSes that they buy, which mostly don’t have reinvestment opportunities.

But it’s another tool in the toolbox, along with PEMS, which makes it incrementally more likely that they are able to deploy a higher percentage of their free cash flow going forward. 🧰

If AMD Stumbled, Who Would Try to Buy It? 🤔💭

This is pure speculation.

Pure, uncut, let’s just think about it, man.

Who would benefit most from acquiring AMD?

A roughly $330B market cap company would usually be too big to swallow. But in a world of multi-trillion-dollar market caps and trillions in planned AI capex, size alone no longer rules it out.

In fact, AMD may be in the interesting middle: too big for most buyers, but small enough to matter to the giants. A Goldilocks AI-scale asset 👱♀️🥣🐻

The most likely scenario for this to happen is probably not “everything keeps going great and somebody pays up anyway.” It’s more likely some kind of stumble. For example, AI hits a bump in the road, valuations compress, or AMD itself ships a disappointing chip generation or falls behind on its roadmap, and the stock gets punished (📉).

It wouldn’t be the first time Mr. Market went cold on AMD either (the stock had been range-bound between the early 1980s and the mid-2010s! And that’s without factoring inflation.. 😬).

Whoever bought AMD would instantly get scale, silicon expertise, and wafer allocation all at once.

But who would be the most strategic buyer?

I can think of four that may line up and write big cheques (or more likely, issue lots of stock):

Amazon

Microsoft

OpenAI

Anthropic

Let’s take each in turn:

Amazon: Hyperscaler ROICs are likely going down because building warehouses full of GPUs for a handful of big customers isn’t nearly as profitable as what they had been doing with their cloud businesses (highly fragmented buyers, lots of sticky, high-margin software products on top of the bare metal).

To improve their returns, controlling their compute costs and differentiating from the competition are crucial. Google has done it with its TPU program, but it has been working on it for over a decade. It’s not something that is easy to replicate organically on a deadline.

Amazon has been successful on the CPU and networking front with Graviton and the Nitro layer (though that’s not optimized for AI workloads), but it has been struggling more visibly with AI. Trainium seems decently promising, but it’s an iterative game and Nvidia is a fast-moving target. Will Amazon’s in-house team be able to keep up? Even if Trainium gets competitive, Amazon would still have to keep pace not just on the chip, but on the software, networking, and all the other chips and parts of the stack that Nvidia is updating at a rapid cadence.

BUT

AMD is valuable partly because it is neutral. The moment Amazon owns it, every other hyperscaler, and maybe plenty of enterprise buyers too, would start treating AMD as rival-controlled infrastructure. So Amazon would be damaging part of the merchant value of the thing it bought. Could the AWS upside be large enough to offset that loss? 🤔

Microsoft: The situation is similar for Azure, except that Microsoft’s in-house ASIC program appears to be further behind Amazon’s. So the strategic logic is similar: more control over roadmaps, more leverage at scale, potentially more differentiation from other compute providers, and more in-house silicon depth.

But buying AMD would not magically fix packaging, HBM, software execution, or dependence on TSMC. It would transform one layer while leaving several others intact.

OpenAI and Anthropic: OpenAI and Anthropic may become large enough that they decide to build their infrastructure themselves to save on whatever margin they would be paying to hyperscalers and neoclouds, and to build up in-house expertise that may differentiate them from the competition (if they pull it off and execute well).

If either could get their hands on AMD at exactly the right moment (the trick would be doing it when AI-lab stock currency is high and AMD is distressed, not when both are in the dumps), it would differentiate them from labs that don’t have an in-house GPU supplier, total control over product roadmap, and the talent to design better ASICs.

OpenAI has an in-house ASIC effort and a Broadcom partnership for custom accelerators, which makes it easier to imagine as a buyer in theory, even if that same effort also weakens the case for needing AMD at all. But their approach is to try to do EVERYTHING at the same time, so it would be on brand.

Anthropic looks less like a company that wants to own the whole silicon stack itself, and more like one that may prefer to pursue custom silicon through close partners like AWS to maintain their focus on the few things they care most about. At least for now. That may change.

Of the two, OpenAI is easier to imagine. Anthropic is the least obvious buyer of the four, partly because it currently has the smallest market cap.

To be clear, we’re just dreaming. I can also think of many reasons why this would be a bad use of capital, a distraction, the cost of AMD losing neutrality, why AMD isn’t the right asset to solve that problem anyway, why it wouldn’t be permitted, etc.

I think it helps to separate strategic fit from actual plausibility. The company that would benefit most from owning AMD is not necessarily the one most likely to get a deal done. Mega-scale M&A is not clean like that.

⚖️👩⚖️ OpenAI and Google Employees Sign Amicus Brief Supporting Anthropic (including Jeff Dean) + Microsoft

The Pentagon is moving forward with the supply chain risk designation, and Trump has publicly directed federal agencies to stop using Anthropic’s technology.

Anthropic is suing, and employees from OpenAI and Google have filed in support, though the companies themselves haven’t. You can see the filing here. The name that stood out to me is Jeff Dean.

The employees argued that “the technical concerns animating Anthropic’s ‘red lines’ are legitimate and widely recognized within our scientific community.” In particular, they argued that current AI systems are not reliable enough to power fully autonomous weapons because AI models often break in new environments, they are not perfectly accurate at identifying targets, they hallucinate, their chains of thought are often hidden, and their internal workings are illegible.

They also agreed with Anthropic that the Department’s decision violates Anthropic’s right to free speech by “undermining the freedom to engage in public debate about how powerful technologies should be governed.”

It would have been nice if Sam Altman had put rivalry aside and supported the larger principle by joining the case officially, not just with public statements. It’s a bad precedent, no matter who the target is.

Update: Last night, Microsoft filed a brief in support of Anthropic. They write:

First, a temporary restraining order will enable a more orderly transition and avoid disrupting the American military’s ongoing use of advanced AI. Otherwise, Microsoft and other technology companies must act immediately to alter existing product and contract configurations used by DoW. This could potentially hamper U.S. warfighters at a critical point in time. [...]

Should this action proceed without the entry of a temporary restraining order, Microsoft and other government contractors with expertise in developing solutions to support U.S. government missions will be forced to account for a new risk in their business planning. The technology sector powers innovation through interconnectedness, tying together services, products, and infrastructure to tackle tomorrow’s challenges. If a single piece of that interconnected offering (long accepted and supported by the government) can be disrupted by a supply chain risk determination, companies will change the way they approach their commercial and public sector relationships in future. [...]

Further, the Determination, as issued, forces government contractors to comply with vague and ill-defined directions that have never before been publicly wielded against a U.S. company.

🧪🔬 Science & Technology 🧬 🔭

🤖💣 Ukraine’s Military Ground Drones & Robots 🇺🇦

The flying military drones get most of the spotlight, but the ground side of robotic warfare is rapidly evolving in sci-fi directions, too.

The video above shows some of the robots that support infantry, hauling heavy supplies, holding positions with no humans around, laying mines, evacuating wounded soldiers, and conducting missions behind enemy lines that would be extremely dangerous for soldiers.

🧠 Lithium Deficiency May Be Linked to Alzheimer’s Disease (Redux) 💊

Back in Edition #582, which is only in the Neogene era, I covered an interesting study on how lithium deficiency is potentially linked to Alzheimer’s Disease.

My highlights:

A unique deficiency: Among 27 metals assayed in post-mortem metallomics on humans, only lithium was significantly reduced in cortex in both MCI and AD, pointing to disrupted lithium homeostasis.

In mouse models: dietary Li deficiency drove AD-like pathology, which strengthens the case that endogenous lithium may be protective, though obviously mice are not humans. 🐁

Potential therapeutic angle: Unlike lithium carbonate, lithium orotate reduced amyloid binding, letting it act at physiological dose to prevent/reverse plaques, p-tau, and memory loss in AD mice. In old wild-type mice, long-term low-dose LiO dampened neuroinflammation and restored microglial Aβ clearance capacity. 🐭

I’ve been taking 5mg of Lithium Orotate daily for a long time (10+ years? I’m not sure).

This recently resurfaced because Bryan Johnson wrote about it and his self-experimentation:

We’ve spent decades treating lithium as a heavy duty psychiatric tool. New evidence suggests it’s actually a foundational brain nutrient and that Alzheimer’s may essentially be a localized lithium deficiency.

By using the Orotate salt, we can bypass plaque-induced transport blocks and restore brain levels with 1mg.

I’ve been supplementing low dose (1mg/day) lithium for years. More evidence now suggests it was the right decision. [...]

The study unequivocally demonstrated lithium deficiency in the brains of patients with cognitive impairment, providing mechanistic evidence of its role as a driver of disease onset and progression.

It validated our choice of Lithium Orotate as the optimal form of lithium supplementation for preventing and slowing the progression of dementia.

Lithium has long been a foundational ingredient in my protocol, utilized in a low-nutritional dose. This was based on our comprehensive analysis of various population studies supporting its safety and potential benefits for brain health and mental well-being.

I had similar thoughts when I began supplementing.

I started after reading research on lithium's natural variability in drinking water — areas with lower levels tended to have higher rates of depression and other mental health issues — and its role in boosting BDNF and neurogenesis. I couldn't know my exact intake from food and water, but putting a floor on it seemed like a nicely asymmetric bet.

5mg of lithium orotate is nowhere near psychiatric doses, even if it may be more than many people get naturally from food and water. There’s a fair bit of natural variability depending on where you live and what you eat and drink.

‘Lithium’ is a loaded word, but you're already consuming it, you just don't know how much, or whether a little more might help.

Establishing a direct mechanistic link: beyond its known effects on mood and well-being, the study forged a direct and mechanistic and progressive connection between lithium brain deficiency and cognitive impairment, including Alzheimer's disease.

Optimal form of lithium: the study revealed that lithium orotate, the specific form of lithium salt I have been using for years, is superior in avoiding blockage by existing plaque, thereby achieving the highest bioavailability, greatest plaque reduction, and cognitive restoration in previously lithium-deficient mice with pre-existing cognitive impairment.

That’s still mouse-heavy evidence, not a human prevention trial, but we should definitely do human studies ASAP.

🧭 How GPS Jamming & Spoofing Affects Ships ⚓

Another aspect of modern conflict is that the battlefield now reaches into civilian navigation systems too:

Within 24 hours of the first US-Israeli strikes on Iran, ships in the region’s waters found their navigation systems had gone haywire, erroneously indicating that the vessels were at airports, a nuclear power plant and on Iranian land.

The location confusion was a result of widespread jamming and spoofing of signals from global positioning satellite systems. Used by all sides in conflict zones to disrupt the paths of drones and missiles, the process involves militaries and affiliated groups intentionally broadcasting high-intensity radio signals in the same frequency bands used by navigation tools.

Modern war doesn’t just blow things up. It also makes ships think they’re at airports. 🛫🚢

While it’s perfectly possible to navigate without GPS, it’s certainly harder and less safe:

On highly automated, modern ships, GPS interference can be hard to detect. And while it’s perfectly possible to navigate using alternative tools, including radar, inertial systems such as accelerometers and gyroscopes, visual watchkeeping, and celestial navigation, younger mariners are often less familiar with these techniques and tools.

It’s a similar situation to how few young people today know how to drive a stick shift car, according to Bockmann. “It takes away all the bells and whistles, and it makes you go back to old school ways of navigating,” she said.

Another reminder that whatever capabilities we don’t exercise eventually start to rot.

A weird side effect of this spoofing is that various companies track the positions of ships to ensure compliance with sanctions or to make sure they stay within whatever parameters their insurance covers. So when the signal from a ship pops up in Iran, banks and insurers get flagged, and it creates a bureaucratic mess.

🎨 🎭 The Arts & History 👩🎨 🎥

🖼️🔬 How Do You Authenticate a New Rembrandt? 🎨🔍

What counts as a ‘new’ Rembrandt, anyway?

Not new paint. New certainty.

Vision of Zacharias in the Temple was treated as a real Rembrandt in 1898, kicked out of the canon in 1960, then disappeared into private hands for 65 years before the Rijksmuseum got to study it and decided to allow it back in the canon. 🔄

The verification story is the coolest part.

They dated the oak panel with dendrochronology, used macro X-ray fluorescence to map the pigments, compared the paint layers and brush handling to other early works, found changes made during the painting process, and examined the signature with microscopy and infrared. The signature appears to have been put into wet paint, which is more convincing than “someone wrote Rembrandt on it later.”

BUT

This made me think of three films about paintings: The Lost Leonardo, Tim’s Vermeer, and The Last Vermeer. (I highly recommend the first two, and the last one is decent)

They are all, in different ways, about how slippery authenticity can be once money, prestige, and narrative enter the room.

I can’t help but wonder if this could still be some wildly elaborate and convincing fake 🤔 My guess is probably not. Those films just make it hard to keep the possibility at absolute zero.

If AMDs fortunes fell away, I’d suspect Broadcom would be the best fit to buy them. They’d be able to combine their other areas with the GPU and CPU and make a success of the whole system like Nvidia have.

Loved "Tim's Vermeer"!

Hope all is well Liberty