92: Mark Leonard's 2021 Letter!, Payments 101, 5 Layers of Roblox, Forget EV/TAM here’s P/FAAMG, How Affirm Works, Obvious Stuff, and Prison Mind-Chess

"Human variance in age and lifespan is far greater than chronology suggests."

Happiness doesn't lead to gratitude. Gratitude leads to happiness.

—A.J. Jacobs (I think — but like most quotes, I’m sure it’s an old idea…)

I hope you enjoyed 𝕊𝕡𝕖𝕔𝕚𝕒𝕝 𝔼𝕕𝕚𝕥𝕚𝕠𝕟 #𝟚 yesterday (interview with Koyfin co-founders).

It was a lot of work to put together over many weeks, but also fun. There’s many more things of that nature I’d like to do, I just need to find the time and energy (right? Sometimes you have the time, but just, eeeeh, productive work isn’t happening).

🛀 Constantly re-learning and remembering the basics is where most of the value is, both in investing, and in life generally.

Everybody's looking for the secret, but if it existed, it long ago would've leaked and stopped being a secret. So it’s all obvious stuff, but simple doesn’t mean easy.

🛀 You could spend all day at the casino and not learn much about how to build wealth.

If you make money without understanding how, you'll likely lose it without understanding how. Most people who win big at the casino don't suddenly get religion and quit while they’re on the top.

They lose it all, and more, chasing that dopamine rush.

🤓 One of the benefits of having English as a second language is that I can pick and choose from whatever idiom or local variant I like most and mix-and-match, because it’s all not my language and foreign to me anyway — it’s not like I’m pretending to be something I’m not; I’m not from any of those English-speaking areas.

I can call someone “mate” and say “bloody hell” and “awesome dude!” all in the same sentence, whatever, I’m my own English-speaking jurisdiction.

⛓ A discussion of how much criticism Buffett gets from some people reminded me of an important, often overlooked aspect of this — and it applies to almost everything once you start looking for it — as people focus on facts and not enough on social context and our human evolutionary tribal baggage:

Humans are social animals. Attacking the top dog is a way to increase your social status by association. Also, social status is largely relative, so if you drag someone else down, you are raising your own standing in the eyes of many.

That's why so many will subconsciously do it to people like Buffett, yet others who are much more deserving of reprimand lower down the food chain only get a fraction of the reproach.

It happens with people, but also with non-human institutions (like companies, brands).

🎧 I was listening to the Cortex podcast, and around this time in it, they discuss how people change over time and how it can be hard to have perspective over long periods of time in our life.

CGP Grey brings up a concept that I find very thought-provoking, the idea of ‘decade-death’.

The idea is that after a decade, you’ve basically changed/evolved so much that the person you were back then is now dead (a decade is just a round number, but it’s can be shorter for some, longer for others).

Now the lawyers in the audience will point out all the ways in which this isn’t literally true in every aspect, and I get that, but I also think there’s a lot to the idea, and we should see ourselves — and others — as more dynamic and fluid than we typically tend to.

If I could somehow have myself from 10 or 15 years ago, and have both my current self and my old self look at various problems, situations, decisions to make, people, etc, I’m pretty sure we’d deal with things like two different people would, in many ways, not like exactly the same person (and that’s good — if you’ve stopped growing, you should question why that is and figure out how to get unstuck).

Also, clearly, some people change/evolve a lot more than others. It reminds me of an old quote by Eliezer Yudkowsky:

People with highly varied lives who repeatedly encounter difficult problems creating skill gain, may have effectively 10 or 50 times the life experience of somebody who's been repeating the same day over and over for decades.

There are 300-year-old vampires walking among us in the guise of free-loving serial entrepreneurs who have since taken up angel capital and opened their own martial arts dojo, and others who've lived less than 1000 non-duplicated days (< 3 years) since puberty. Human variance in age and lifespan is far greater than chronology suggests.

Now clearly, if you meet someone who you haven’t seen in 10 years, but they are one of these people basically living the same day over and over again, they may not have changed much. But if you meet someone who’s constantly learning, growing, introspecting and trying to figure how to be better, they’re not going to be the same 5 years later.

I don’t know if it counts as “death/rebirth”, but it counts as something.

It’s partly why it matters who you partner with in life, and that you evolve together (or stay static together — but that I don’t recommend if you can avoid it).

I also really like in that podcast when CGP Grey says something like: “Yeah, my wife and I joke about this — we didn’t get married, some kids got married, and now we live together.” Such an interesting way to think about this.

P.S. Riffing on this, you could also think about it from a purely biological point of view. Most of the cells in your body aren’t the same vs x years ago, you are literally in large part a different person (though that also brings up what is “you” — I’d say it’s the patterns of your cells more than the specific cells themselves, and your DNA tries to maintain that pattern, plus longer-lived cells in the brain, etc).

Bloody hell, mate, that’s just awesome to think about, like, dude.

Investing & Business

Mark Leonard’s 2021 Shareholder Letter 💫 (Constellation Software)

When I saw that there was a new letter, the first one since 2017, it felt a bit like a mix of Xmas and a sighting of Halley’s Comet:

It’s not totally out of the blue because the past few AGMs already touched on these themes and showed that management was thinking about these things, but it’s still surprising to see this type of course-change in our world of incrementalism, half-measures, and people afraid to change their minds.

Mark writes really well, so you should read the whole thing (it’s a short one, only 1.5 pages), but here are some highlights with my thoughts:

I used to argue that we needed to maintain our hurdle rates because dropping them for a few marginal capital deployments would cause the returns on our entire portfolio to drop. The evidence supported my contention, so we kept the rates high for small and mid-sized vertical market software ("VMS") acquisitions and made very few exceptions for large VMS acquisitions. The by-product of that discipline has been a perennial inability to invest all of the cash that we generate.

If you’ve read the past letters, this is the “magnetic hurdle rates” theory.

I have stopped arguing. I have converted, and with the fervour of the newly converted, I am busy demonstrating my new-found faith.

The obvious first step is to stop special dividends in all but the most compelling circumstances. That decision was made by our directors at Friday’s CSI board meeting. [...] if we are successful in finding better uses for our FCFA2S, the quarterly dividend will also be sacrificed

First, that’s good writing. Second, that’s what you want in a CEO. Someone who cares more about figuring things out and being correct than about being consistent or winning arguments. It’s a lot like this thing that I keep as my pinned Tweet:

Back to the letter:

We will continue to invest most of CSI's FCFA2S in small and mid-sized VMS acquisitions at our traditional hurdle rates. [...]

we are working on two initiatives: 1) increasing the number of very large VMS businesses (i.e., those requiring multi hundred-million-dollar equity cheques) that we pursue, and 2) developing a circle of investing competence outside of the VMS sphere.

This is big! They already said in recent years that they were increasing their efforts to go after larger VMSes, but this doesn’t sound like just an incremental twist on the intensity knob from 5.5 to 6.5, this sounds like a full Spinal Tap moment.

We have invested less than 10% of our FCFA2S in this segment, making only three

large VMS acquisitions during our entire 26 year history.Between 40 and 70 large VMS businesses are sold each year [...]

We are building a small, dedicated team at head office to pursue large VMS acquisitions and to work with M&A brokers. If we drop our hurdle rates for these acquisitions, I believe that competent and diligent M&A brokers will include us in more auctions.

Mark mentions some of the advantages for some of these large VMSes in going with Constellation rather than a private equity buyer that will flip them 3-7 years later, and mentions that it can be a good fit “even if their ultimate objective is to eventually be a publicly listed company”. This has shades of the Topicus-TSS acquisition/spin and shows how creatively they are thinking about this.

Will we end up with a constellation (pardon the pun) of full and partial spin-offs and, maybe even channeling Malone/Maffei, tracking-stocks someday?

If we are successful in acquiring one or two large VMS businesses per annum, then I anticipate that CSI's return on investors’ capital will decrease, but we will not have to return any of our free cash flow to shareholders.

As a shareholder, I welcome this because I trust them to still have a decent hurdle rate and to often over-deliver, but most importantly, to adjust things if they find out that their approach doesn’t work out as well as they expect it to. I know that they aren’t empire-building or doing this for reasons that aren’t aligned with my interests, so I’m glad they’re trying new ways to create value.

But the other big part of this is also intriguing:

we are trying to develop a new circle of competence. We are seeking attractive returns, a sustainable advantage, and the ability to deploy large amounts of capital

outside of VMS. That will require highly contrarian thinking and is likely to be uncomfortable in the early going. Hopefully, we have built enough credibility to warrant your patience as we explore new and under-appreciated sectors.

This is more out-of-the-box thinking, and I love it. I wouldn’t want most companies that are specialized in an area to do this, but once again, trust is an important ingredient, and I trust that they’re doing this with their eyes wide open to the pitfalls, and their brains fully switched on to figure the best ways to go about this and experiment in ways that aren’t bet-the-company, but rather more like R&D.

I’m wondering if the way to get into a new industry is, after studying it a lot, to make a “platform” acquisition that becomes the seed of a new group within the company, and using its pre-existing expertise, that platform can then do M&A and help head-office learn more.

Obviously, you only scale up what works, and there’s always risk of failure with bold experiments…

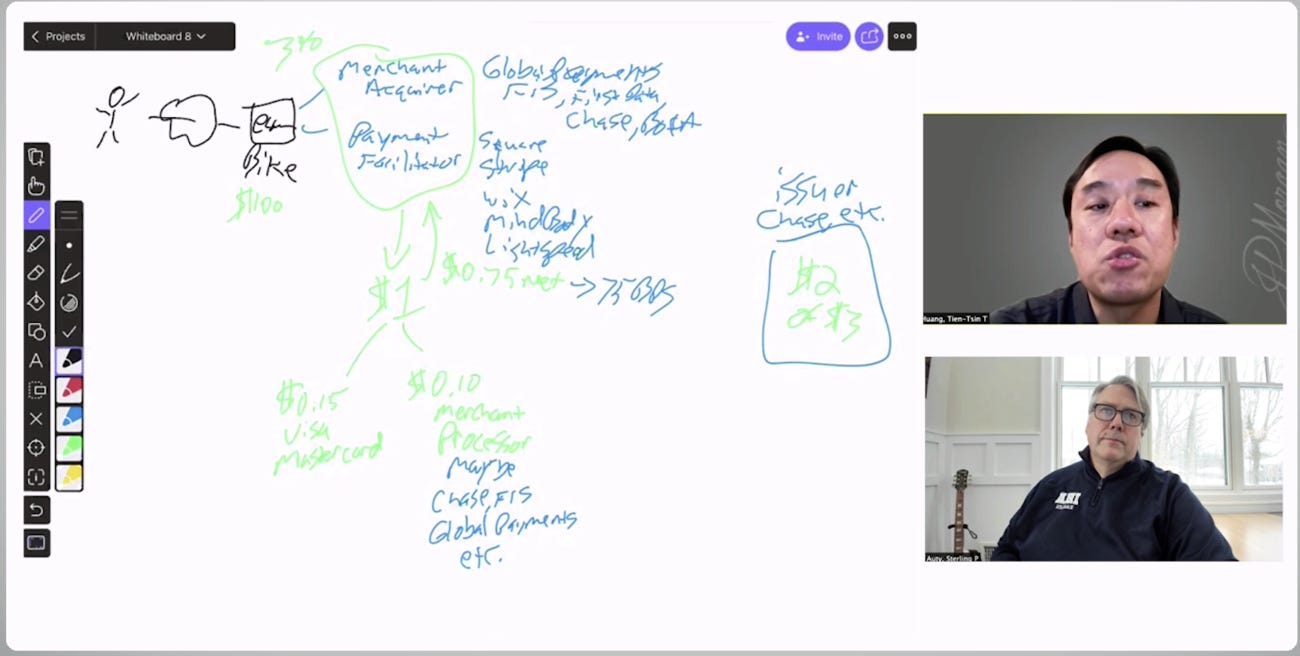

Payments 101 with Tien-Tsin Huang

If you want to understand a bit better the basics of this very complex business, this 60-minute presentation between Sterling Auty and Tien-Tsin Huang, the lead payments analyst at JPM, is a really good primer. The first half is explaining the structure and players in payments, and the second half is Q&A:

Payments Presentation by JP Morgan Chase analysts (I wish they had a way to watch at more than 1x)

And you know it’s good, because it was recommended by The Dentist on Twitter (sounds like a film villain, doesn’t it?).

And if you don’t have the time to watch the video, Secret Capital has a good recap thread.

Software is taking over payments. Consumers want to interact with software and not banks. Historically payments were integrated with banks who would own the relationship.

Over time, they started to work with payments companies working with merchants. Banks partnered with these software companies and offered the payments piece, and sent a cut to the software providers.

Payment facilitators (payfacs), like Square, Shopify, etc. now offer the payments piece and earn the economics of it. Before SMBs would engage with banks when they started, so it was easy to sell the payments piece.

Now companies are more concerned with the front-end tech of the business, so these tech companies sell the payments now. Ex: before even getting a bank account, an entrepreneur will likely set up a site on Shopify, so SHOP has distribution. [etc]

Forget EV/TAM, Here’s P/FAAMG

Some bold thinking by Packy McCormick. I like it, it’s thought-provoking and just outside-the-box enough to add something to the mental mosaic:

Averages are obviously imprecise but they paint a pretty clear picture here: you can abstract away a lot of complexity by thinking about startup valuations as the probability that they can grow as large as Facebook, Amazon, Apple, Microsoft, or Google. The higher the valuations of the biggest tech companies, the higher the potential valuations of any startup.

Take Clubhouse, for example, which was recently valued at $1 billion before earning a dollar. Helllloooo bubble, amiright? Nope. $1 billion means investors are pricing in a 1/770 shot it can become the next Facebook, a 1/100 shot it’s the next Snap, or a ~1/50 shot it’s the next Twitter.

Adding credence to the P/FAAMG methodology, FAAMG haven’t only proved that companies can get really big from a market cap perspective, but also that their eventual success isn’t clear from looking at the early financials. Facebook and Amazon’s financials looked silly early on -- Facebook not monetizing for a long time, Amazon intentionally keeping itself unprofitable -- but their strategies have been proven right in the long-term. [...]

This also works within verticals; valuations can be viewed as the probability that they become as large as the largest company in the space. That explains why some verticals get hot when its biggest companies break out, like Stripe in fintech or API-first or SpaceX in space tech.

You can read the whole thing here.

Roblox: 5 Layers of Business Model Nirvana

Good thread by Ben Gilbert (of the Acquired podcast) summarizing the ways in which Roblox’s business model is attractive:

1. Like any piece of digital content, there are zero marginal costs to make a copy.

The cost of content creation is now entirely decoupled from the value it can create, which in the land of bits, scales solely with audience size.2. Like any piece of software, there are zero "reuse" costs by the same user.

If content's downside is that it typically is consumed once, software is way better can be reused over and over! This decouples creation costs (coding) from value delivered on yet a 2nd axis (time).3. Like any piece of software on the internet, there are zero distribution costs. This adds to the power of zero marginal costs, where it is not only free to copy the software for a second user, but also free to send it to them.

4. On top of all of this, because most transactions actually happen in Robux, there are zero transaction costs for most in-game purchases. (!!) This means that Roblox can keep all those would-be-lost CC fees in the system and continue to compound those dollars over time.

5. And, for a cherry on top, this is an unbelievable "float" business. Roblox gets paid for the purchase of Robux long before they end up paying out to the developer.

Curious about how Affirm works?

Was trying to understand the BNPL space a bit better, and I thought this was a good write-up that looks at pros and cons and isn’t just breathless cheerleading:

If you have a sub to The Diff, this post by Byrne Hobart is also great:

Not the same company, but this presentation by Hayden Capital on Afterpay in Australia also covers a lot of stuff:

The New Signal Advance

Science & Technology

Fortune Special with Bill Gates as Guest Editor

Lots of interesting stuff in there, including some of the less-sexy-but-damn-important topics that often get overlooked in favor of solar and EVs:

Gates also posted on his blog about his new book:

Mind-Chess in Prison

Via Gary Kasparov, an interesting piece about chess in prison:

being in prison during the COVID-19 pandemic is the worst. It’s like being at the center of one of those Russian nesting dolls—a box within a box within a box. Social-distancing policies limit our access to recreation yards, the dayroom, classes, and phones. Some days we spend roughly 23 hours in our 6-by-10 cells. And on top of everything, board games—including chess—have been completely banned. This situation has forced us to create a new approach to a classic game. [...]

Wally and I live on the same row, two cells apart from each other. Since we’re in shouting distance of one another, we decided to play the game in our respective cells. We both set up our chess boards and used algebraic notations to tell—or yell—our moves to one another. [...]

But prison is loud, and the letters B, C, D, and E sound very similar over a ruckus. To avoid confusion Wally and I came up with a nomenclature for those letters: “alligator” for A, “baseball” for B, “constellation” for C, “dinosaur” for D, “elephant” for E, and “golf ball” for G.

The Arts & History

Mommy

Someone just reminded me of the giant spider sculpture at an art museum in Ottawa... Found one of my old photos.

It was made by Louise Bourgeois, and it’s called “Maman” (Mother, or Mommy).

I don't know if I like that better, or the giant jellyfish at the natural history museum:

There’s also this freaky one that I saw a few years ago in Montréal.

Hey, great work!

What's the source of the Eliezer Yudkowsk quote " People with highly varied lives who repeatedly encounter difficult problems creating skill gain...."

Google didn't have any results, and DuckDuckGo got me back here :)